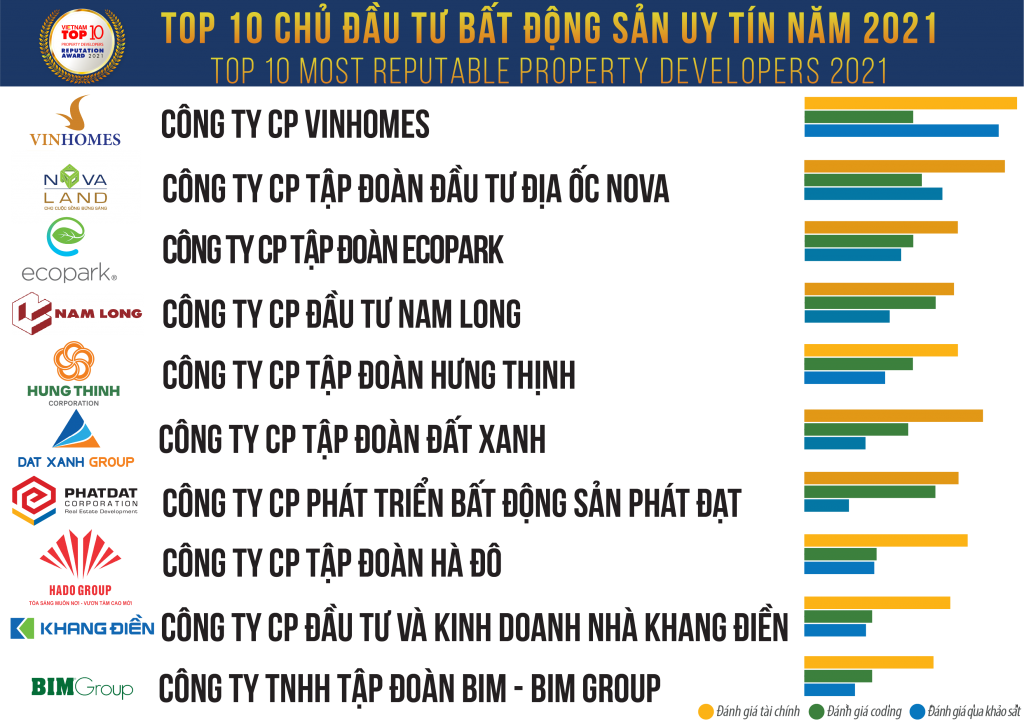

On March 19, 2021, Vietnam Report Joint Stock Company (Vietnam Report) officially announced the Top 10 Most Reputable Property Developers 2021.

Top 10 most reputable property developers are evaluated and ranked based on 3 main criteria: (1) Financial capacity as indicated in the latest annual financial statements; (2) Media credibility assessed using the Media Coding method – coding articles about the company on influential media channels; (3) Survey of stakeholders, conducted in February and March 2021.

List 1: Top 10 Most Reputable Property Developers 2021

Source: Vietnam Report, Top 10 Most Reputable Property Developers 2021, March 2021

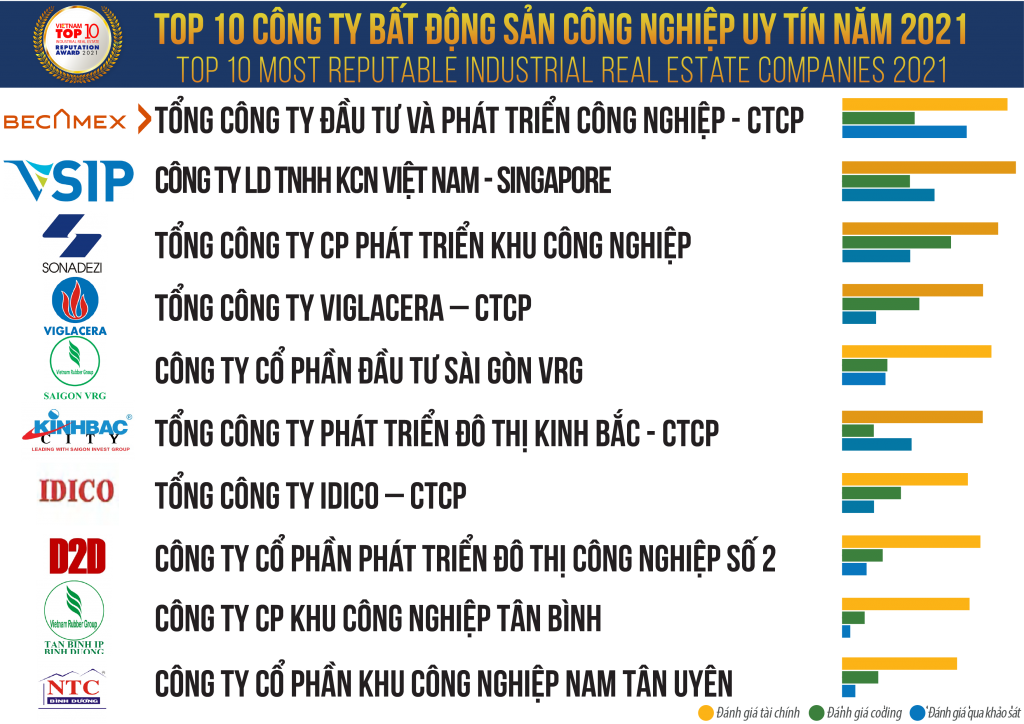

List 2: Top 10 Most Reputable Industrial Real Estate Companies 2021

Source: Vietnam Report, Top 10 Most Reputable Industrial Real Estate Companies 2021, March 2021

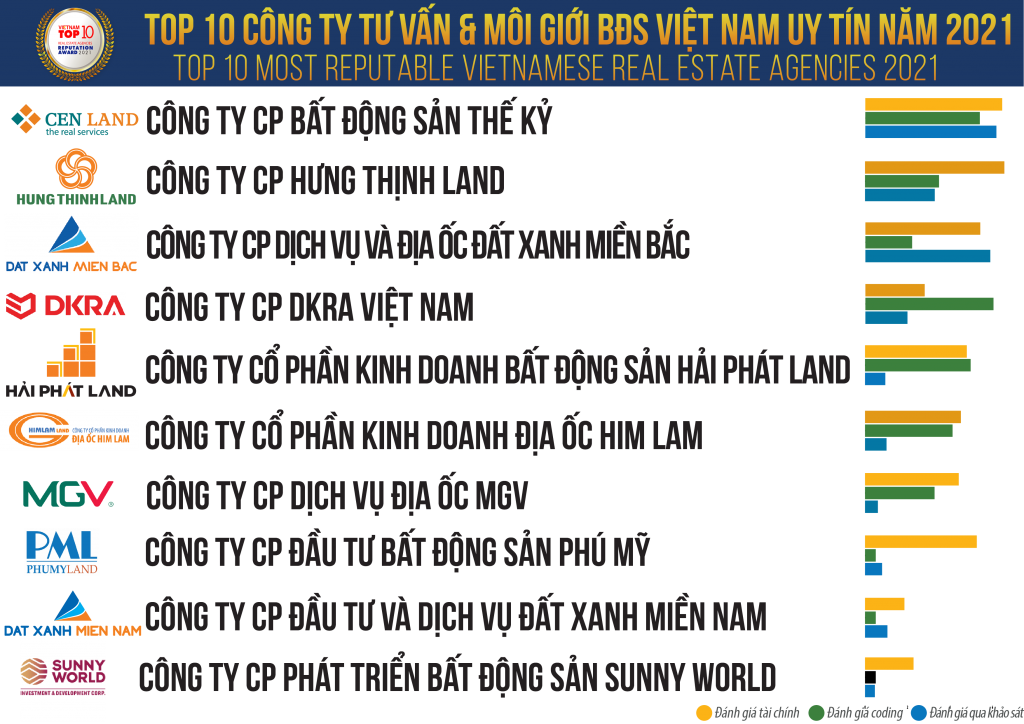

List 3: Top 10 Most Reputable Vietnamese Real Estate Agencies 2021

Source: Vietnam Report, Top 10 Most Reputable Vietnamese Real Estate Agencies 2021, March 2021

The real estate market in 2020 faced numerous challenges and fluctuations as property development was negatively impacted by the Covid-19 pandemic.

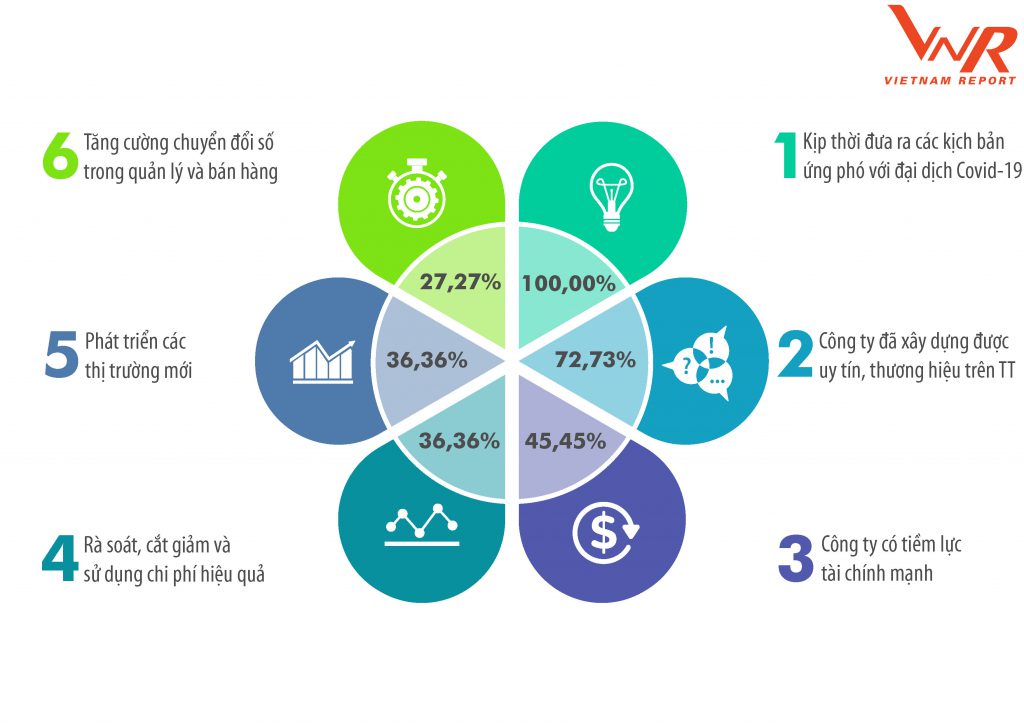

The survey of property developers by Vietnam Report identified 6 factors that enable businesses to overcome difficulties caused by the Covid-19 pandemic: Prompt development of scenarios for response to the pandemic (100%); Building a strong reputation and brand in the market (72.73%); Strong financial health (45.45%); Review for effective cost cutting and management (36.36%); Development of new markets (36.36%); Stronger digital transformation in management and sales (27.27%).

Figure 1: Top 6 factors that enable businesses to overcome difficulties caused by the Covid-19 pandemic

Source: Vietnam Report, Survey of property developers, February and March 2021

Media credibility assessment of property developers

As analyzed above, building a strong reputation and brand in the market is one of the factors to enable property developers to overcome difficulties avid the Covid-19 pandemic.

Accordingly, nearly 54.4% of surveyed companies were covered by media at least once a week, where Vinhomes was the one having the largest number of coding units.

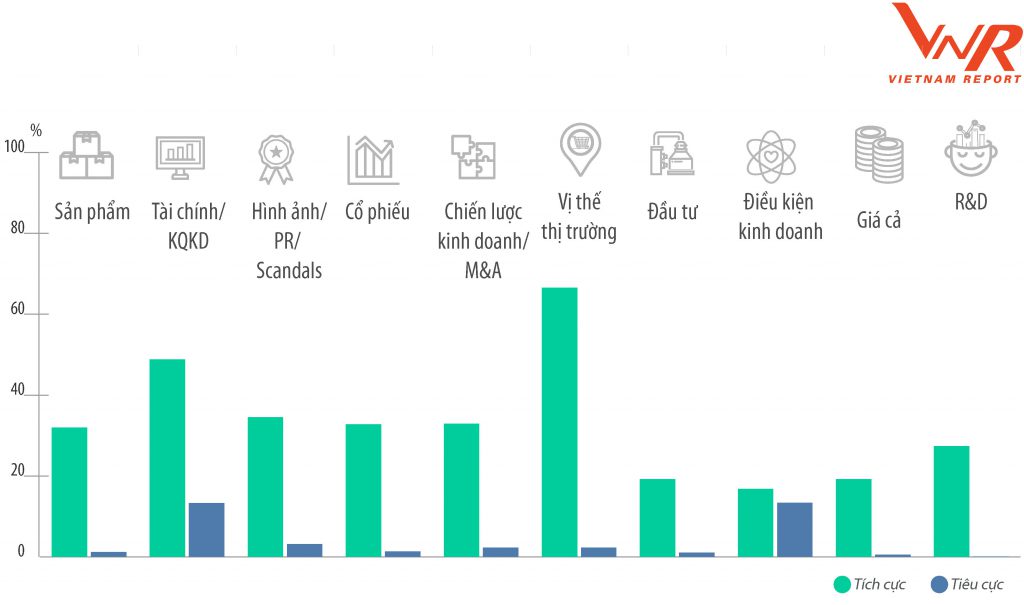

In terms of corporate image diversity in the media: 65.82% of surveyed companies were covered in 10/24 themes, with Novaland to be most widely cited in 21/24 themes. The top 5 most discussed themes are: Products, Finance/Business performance, Image, Stocks and Business Strategy/M&A.

Figure 2: Rate of positive – negative news for the top 10 themes in the media

Source: Vietnam Report, Media Coding data of property developers from January 2020 to January 2021

Active media appearance of a company is also considered as an important factor affecting the risk management of media credibility of the company. As a rule, to ensure accurate information and increase media credibility, at least 1/3 of information about a company in the media needs to be sourced from such a company and its senior leaders (member of the Board of Directors/Board of Management). However, the Media Coding analysis results show that the amount of information sourced from surveyed companies during the study period only reached 23.6%.

In terms of information quality, an enterprise is rated as “safe” when the proportion of positive and negative news in the total amount of coded information is 10%, but the “most ideal” threshold is over 20%. In the real estate industry, this proportion was 10% for 73.42% of surveyed companies. It should also be noted that the more media appearances a business has, the more difficult it is to achieve the “most ideal” threshold, especially when it comes to maintaining this rate over the course of 12 months in a year.

Monthly information changes: Despite the impact of the pandemic, information in the real estate industry was strictly controlled, with negative news to reach higher than the “safe” level in March, August, September and November. The rate of positive news increased higher in ending months when the market recovered.

Besides, enterprises also need to maintain a certain proportion of information about their representatives (BOD Chairman or Chief Executive Officer), usually at 20%. However, media presence of representatives of property developers remains limited in the number of face-to-face interviews and articles with quotes from their representatives.

Regarding the information structure, most businesses believe that intensive communication is effective to widely promote their products. However, for proper reputation management, it is necessary to have a reasonable information disclosure plan to expose the public with its best corporate elements/strengths. Four main themes are most often of public interest: Customers/Products; Personnel; Improvement/Development; Social/Social Responsibility. Businesses that have effectively leveraged discussions around these themes include Vinhomes, Novaland, Ecopark …

Top 5 challenges and factors that would drive disruptive development of the real estate market in 2021

The biggest challenges faced by the real estate market in 2021 are: (i) Unpredictable developments of the Covid-19 pandemic; (ii) Condotel policies: So far, there has been no legal document on Condotels, Officetels or shophouses, etc., leading to different practices between one province and another; (iii) The process of licensing, appraising and approving construction projects is prolonged and complicated with different steps; (iv) Credit limits due to non-changes to the current regulations mean that enterprises have limited access to cheap capital; and (v) Tax policies such as those on related-party transactions remain complicated, not providing property developers with a peace of mind. Such a policy aims to prevent transfer pricing, not transactions in the real estate market, while the real estate market eventually suffers from those undesirable effects.

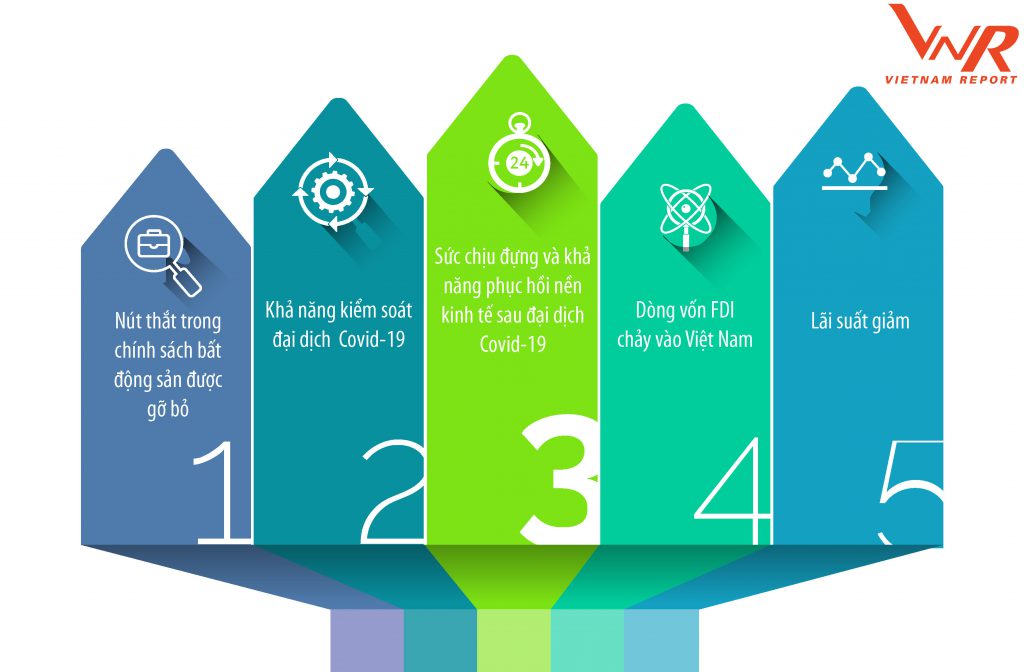

The survey of real estate experts and companies by Vietnam Report using the 5-point Likert scale has indicated the top 5 factors that would drive disruptive development of the real estate market in 2021, namely: (i) Removing bottlenecks in real estate policies; (ii) Containment of the pandemic; (iii) Post-Covid-19 economic resilience and recovery; (iv) FDI inflows into Vietnam; (v) Lower interest rates.

Figure 3: Top 5 factors that would drive disruptive development of the real estate market in 2021

Source: Vietnam Report, Survey of real estate experts and companies, February and March 2021

First, the bottlenecks in real estate policies should be removed. In 2020, the real estate market slowed down. This was partly attributed to overlaps between laws and regulations, especially in 2019-2020. Fully aware of this, government agencies and legislative bodies issued circulars, decrees and instructions to address questions and removed barriers left over in 2019-2020. Therefore, more enabling conditions will be in place in 2021 in terms of legal procedures governing the real estate market. These include Decree 25, Circular 21 by the Ministry of Construction, Resolution 164 on addressing legal issues in delivery of real estate projects, and Decree 148 on revising a number of decrees on the implementation of the Land Law that entered into forced from February 8, 2021, including important provisions related to thousands of projects having interlaced land plots that are expected to remove the bottleneck of supply shortage. Besides, according to expert assessment as documented in the Vietnam Report’s survey, the biggest enabling factor is the public investment disbursement policies, seen as a key solution to delays, and public investment will be facilitated strongly in 2021, same as in 2020.

Second, it is the extent to which the pandemic is contained. The Covid-19 outbreaks reduced the purchasing power of the whole economy in 2020. Apart from its impacts on tourism, sale of agricultural products and trade, the purchasing power in the real estate industry also dropped significantly. Except for certain provinces such as Ho Chi Minh City where the purchasing power grew despite increasing housing and land prices, market developments in others, including Hanoi, followed the downward trend. COVID-19 vaccines have been rolled out, yet, even the US, the world’s largest producer of vaccines, still projected that the pandemic can only be contained by the end of 2021 and its economy can rebound to normal levels in 2022. In other countries in Europe or Asia, the pandemic developments remain complicated.

Third, it is economic resilience and recovery. As a general rule, the market normally goes through ups and downs in a sine wave, and it dropped to a very low level in 2020. Vietnam’s economy is in the recovery phase, recording a GDP growth of 2.91% in 2020, a 10-year record low. In the Asia Pacific region, Vietnam is one of three countries, apart from China and New Zealand, having positive growth. This is, of course, a low growth rate, yet making Vietnam to become one of the few economies with positive growth given strong impacts of the pandemic globally. Vietnam will further recover in 2021 and its GDP growth as targeted by the Government is about 6%. This is an ambitious target for the Vietnamese economy but it is feasible. Given Vietnam’s economy is expected to recover and grow, the local real estate market will also rebound when there are favorable opportunities and conditions.

Fourth, it is ODA flows into Vietnam. Given the US-China trade war and Vietnam’s strong commitment to new generation FTAs, its location in a dynamic region, its social and political stability, and Vietnamese’s aspiration to rise are the three factors that invite capital flows to Vietnam. Therefore, FDI investment in the real estate sector is forecast to increase sharply in the near future since a large amount of capital from newly established property development funds is ready to be poured into Vietnam while exports will expand under signed trade agreements, tourism activities will be gradually growing, more foreign investors will be allowed to enter Vietnam, and macroeconomic and microeconomic policies will be flexibly adjusted to create a driving force for the real estate market to be heating up.

Fifth, interest rates are negatively adjusted. When the gold market presents numerous risks and the foreign currency market is tightly managed without huge interests, it is inevitable that the cash flow will be strongly driven to the stock market. Many investors take loans to invest in stocks. According to expert opinions as surveyed by Vietnam Report, if the stocks continue to grow strongly, it may lead to a stock market bubble. However, if all the legal barriers to property development are removed, the real estate market will recover, with adjustments in place towards a more balanced development. At the time, compared to stock investment, real estate investment would become more predictable, although the resort property segment is strongly affected by the pandemic. Regarding the Government’s policies, the low interest rates have greatly driven an increase in both supply and demand on the real estate market, including real estate traders and builders since they can access to low-interest bank loans, thus reducing their capital costs and facilitating property construction. Property buyers also benefit from getting loans at a lower interest rate. The low interest rate policy is an enabling condition for the real estate market. This should be maintained, in addition to efforts in inflation control.

2021 real estate market outlook

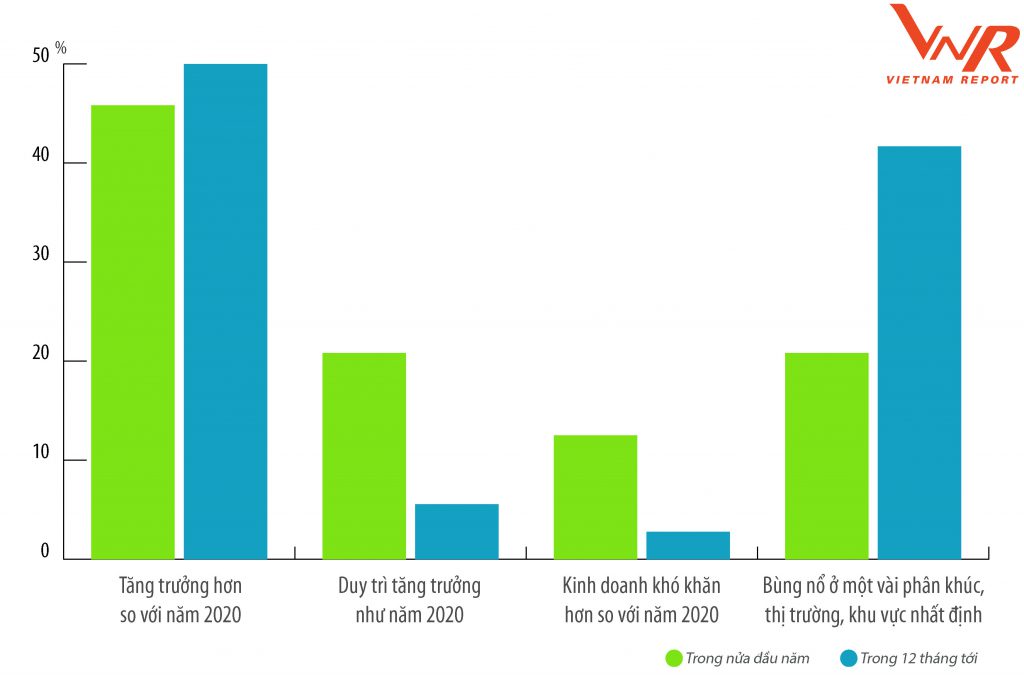

The real estate market outlook in 2021 has not been clearly defined because it depends on assumptions and actual market developments. However, experts and companies engaged in the Vietnam Report’s survey are quite optimistic about the strong recovery of the real estate market. If Vietnam can contain the pandemic, the real estate market will be an important pillar in the country’s economic recovery in 2021.

Real estate experts and companies interviewed by Vietnam Report believe that, in 2021, particularly H12021, the real estate market will continue to recover and grow, even leading to a boom period, in certain segments and regions.

Figure 4: 2021 real estate market outlook

Source: Vietnam Report, Survey of real estate experts and companies, February and March 2021

Market trends by segment of the real estate sector

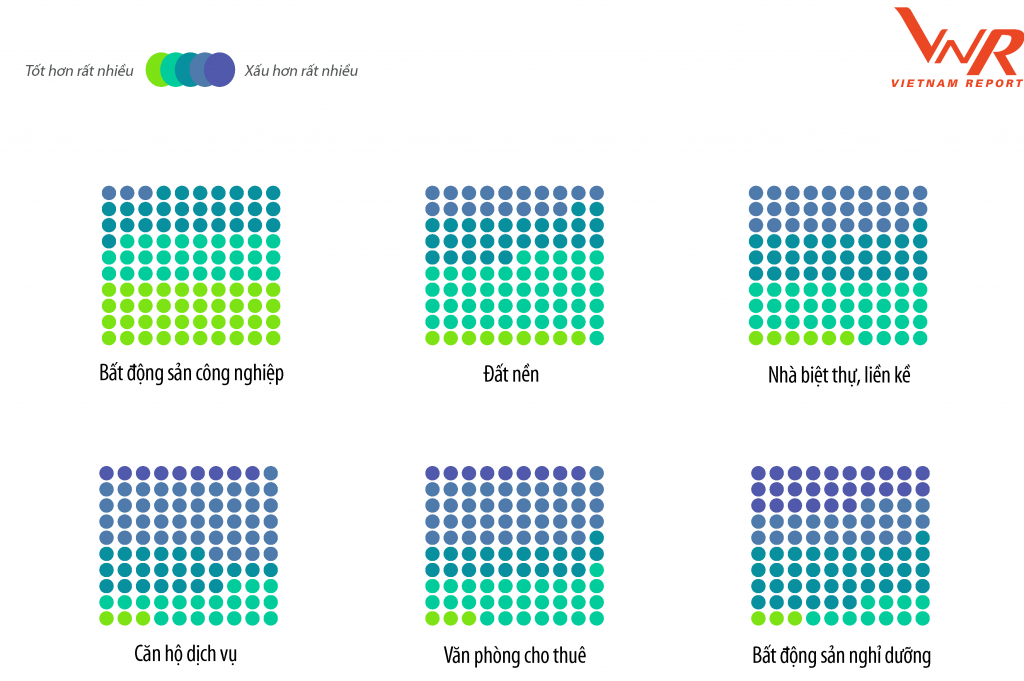

According to real estate experts and companies interviewed by Vietnam Report, some segments that will be further attractive to investment are industrial parks, mid-range apartments priced from VND 25 to 30 million/m2 for real buyers, serviced real estate, housing linked to industrial parks and priced from VND 1-3 billion and mountain resort properties.

Figure 5: Real estate market outlook by segment

Source: Vietnam Report, Survey of real estate experts and companies, February and March 2021

Resort real estate: This is the segment that has been hit the hardest, but in H22021, in case large-scale vaccine rollout, its growth is highly expected. This segment is highly characterized by seasonality and even 6 months of strong growth can compensate for its slowdown in the whole year. Therefore, whether this segment can recover or not depends a lot on Vienam’s Covid-19 containment. During the Covid-19 outbreaks, many resort real estate investors in Da Nang and Nha Trang have encountered difficulties and are silently waiting for the market to fully recover. In the North, many mountain resorts have been developed and this pattern is expected to grow in 2021. Tourist destinations about one- or two-hour drive from a city have become popular as tourists are avoiding long-distance travel or using planes for vacations.

Office building segment: There will be two trend in this segment in 2021: (i) The focus will be on projects that are likely to generate revenue and projects in prime locations and (ii) non-potential projects and new projects to be developed in unfavorable locations will face difficulties and be temporarily “suspended”.

Land lot segment: As one of the real estate products mostly not affected by any factor, this segment is still growing strongly, especially in provinces and cities with planned or large-scale ongoing projects, and in high-growth areas. This is a long-lasting product whose value is always increasing in direct proportion to time time and its scale. In addition, land plots adjacent to large-scale infrastructure projects such as the buffer zone of Long Thanh airport, the corridor of transport infrastructure works, the border areas of emerging industrial parks – are to be affected for development of buffer zones, especially when Ho Chi Minh City is proposing to acquire the corridors on both sides of an infrastructure project for auctioning and development.

Residential property segment for low-income buyers: This is still a high-demand segment, but investors’ interest is low as the profit margin is too modest. For this segment to develop, the Government involvement by encouraging investors and banks to invest more in the low-income housing segment is needed. Stronger investment flows are needed but are slowly pouring in this segment. Therefore, its growth potential will be relatively low in 2021.

High-end real estate segment: In major cities like Hanoi or Ho Chi Minh City, this is an attractive segment that engages many foreign investors.

Industrial real estate: This segment presents development potential in the next 2-3 years as some investors from China and other countries are planning to relocate their production to Vietnam. This is a promising area of investment to all investors. However, investment in the industrial real estate segment should take into account development master plans for industrial parks and transport infrastructure, among others. According to experts interviewed in the Vietnam Report’s survey, there has not been a wave of FDI investment into Vietnam. At this time, there are only a few large foreign investors in Vietnam and this has caused a real transformation. Meanwhile, the trade war between the US and China is being gradually de-escalating. Therefore, the migration of some US businesses into Vietnam may not take place as strongly as planned. Besides, the current industrial real estate market is also much different from that 10-15 years ago. Investors in industrial parks only developed infrastructure, then waited for tenants to come and develop their own factories, which has now changed in Vietnam as investors can also build ready-made warehouses and factories for lease. In addition to investment in factories and workshops, development of warehouses for lease is also an effective form of industrial parks investment.

Agricultural real estate segment: This is another segment that is attractive to many. Thanks to a large agricultural land bank, most provinces in Vietnam have agricultural real estate to offer. Yet, it remains unclear whether investing in agricultural real estate would generate profits as investors are unable to develop agricultural real estate into resort properties, commercial properties or industrial parks. Converting agricultural real estate into other land use purposes is not easy and must be in line with a land use master plan. According to experts interviewed in the Vietnam Report’s survey, agricultural real estate is a potential segment but the current investment in this sector is not as strong as expected.

Upward trend in prices

According to survey findings of Vietnam Report on property prices in 2021, prices will be increasing in most of the segments, except for the resort real estate for which up to 56.25% of surveyed experts and companies believed that prices will remain unchanged and 18.75% of the respondents thought that the prices could be down by 10%.

Experts interviewed by Vietnam Report indicated that it is now hard to predict the extent to which property prices will increase this year as the market developments are currently unpredictable. However, it can be expected that the high-end real estate segment will grow stably with price increase by 5%-10%. Real estate for middle-income earners will also be expanding, provided that the pandemic is controlled, with the prices to increase by 5%-10%.

As for the industrial real estate segment which has attracted lots of attention, time will tell its growth momentum after a massive influx of foreign investors. These investors, before investing into Vietnam, will look at whether other countries and regions would provide better options than Vietnam. It is clear that our neighboring countries, including China, Thailand, Malaysia, Indonesia, Singapore and even the Philippines, are also offering competitive real estate to attract FDI investment into industrial real estate, imposing strong competition to Vietnam. According to 37.5% of experts and companies in the Vietnam Report’s survey, the price growth in the industrial park real estate sector could range between 10% and 20%.

The agricultural real estate segment this year is expected to have a strong price growth, maybe 10%, given a large number of investors and products. With a developing economy like Vietnam, conversion of agricultural land into industrial land, commercial land or residential land is a necessity while it is also important to protect the agricultural sector that forms the backbone of Vietnam’s economy.

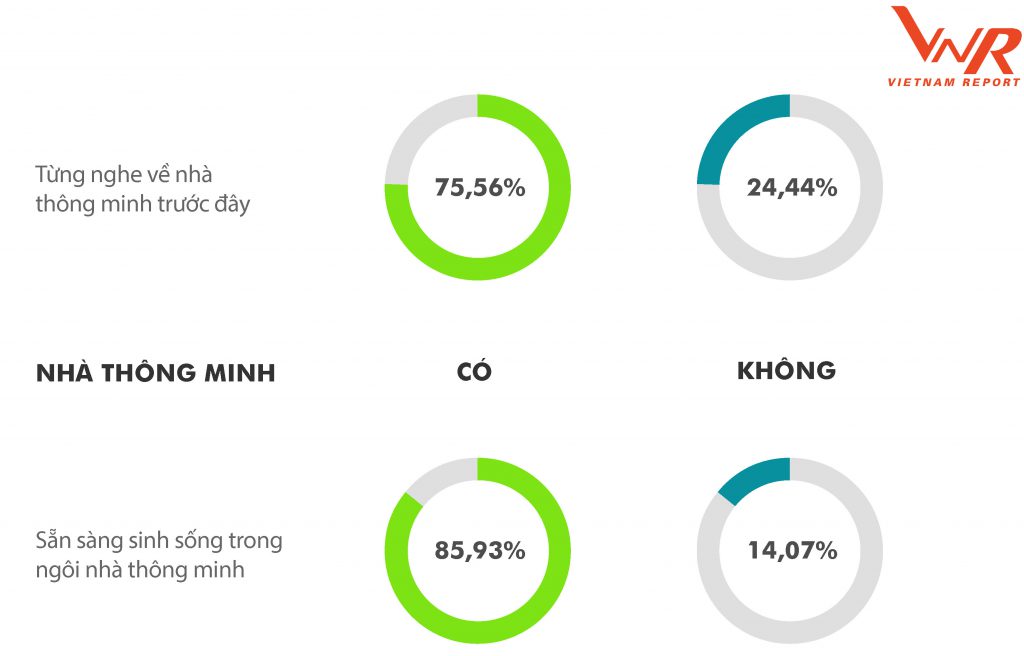

Smart home trends

As indicated by many experts and companies, smart homes will be inevitably on the rise on the housing market in the future. Capturing this opportunity, many investors are promoting smart home development to create a competitive advantage for their projects. With adoption of artificial intelligence (AI) connecting devices on the Internet of Things platform, home owners can manage their properties remotely using mobile apps or directly operate their properties using a smart switch or voice control. In the Vietnam Report’s survey, 75.56% of the respondents have heard of smart homes as a concept and 85.93% of them are ready to live in a smart home.

Source: Vietnam Report, Survey of property buyers, March 2021

According to Statista data, the Vietnamese smart home market was worth USD 83 million in 2019 and the market size is expected to reach about USD 437 million in 2023 for a growth rate of 51.7% in the period 2019-2023.

However, a Vietnam Report’s survey of home buyers has revealed top 4 concerns about smart homes including: Costs; Information security; Performance of smart home features; and Technology reliability. Among these, high costs present the biggest barrier to smart home development, given that development and device installation costs for smart homes usually range from VND 50 million to several billion, so the target buyers of this segment are usually high-income earners.

Figure 7: Top 4 concerns of home buyers about smart homes

Source: Vietnam Report, Survey of property buyers, March 2021

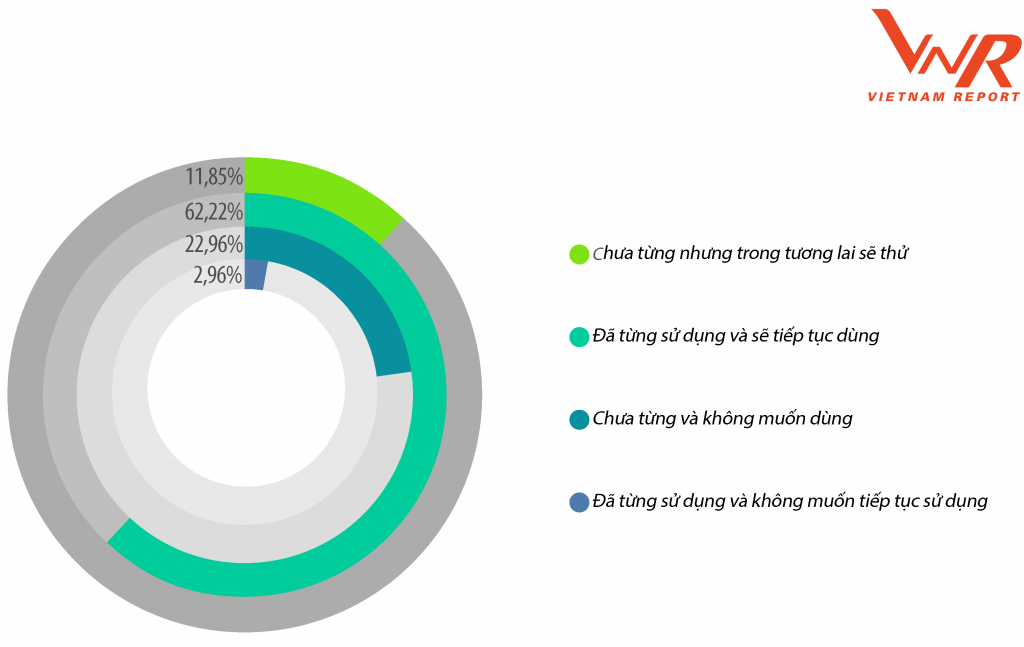

Getting trendy: Online real estate services continue to grow and boom

In the context of the Industry 4.0, technology is seen as the key to drive the growth of business, including property developers. In addition to traditional business models, the digital business models are gradually growing on the market to create a new wave of competition. Currently, there are two types of businesses that develop applications in the real estate industry (protech), which are traditional real estate companies undergoing digital transformation and start-ups companies built on protech platforms. Some real estate companies have developed applications covering an end-to-end process, from product design to official launch.

According to the Vietnam Report’s survey of home buyers in March 2021, the most common information sources used before buying properties are friends and relatives (68.15%), real estate forums and groups (65.93%), real estate websites (35.36%) and real estate agencies (35.36%). In addition, up to 16.30% of the respondents sought information from real estate trading platforms and nearly 2% of them learned information via livestreams. The virtual reality technology allows real estate agents to guide their buyers in virtual visit of properties without leaving their homes, thus avoiding contacts in the context of the pandemic. Research findings of Vietnam Report also show that 22.96% of the respondents have used real estate trading platforms and plan to continue using them while 62.22% have never but will try them in the future. Besides, 11.85% of the respondents have never and do not plan to use them given concerns about security and scam risks.

Figure 8: Comments on property transactions on real estate trading platforms

Source: Vietnam Report, Survey of property buyers, March 2021

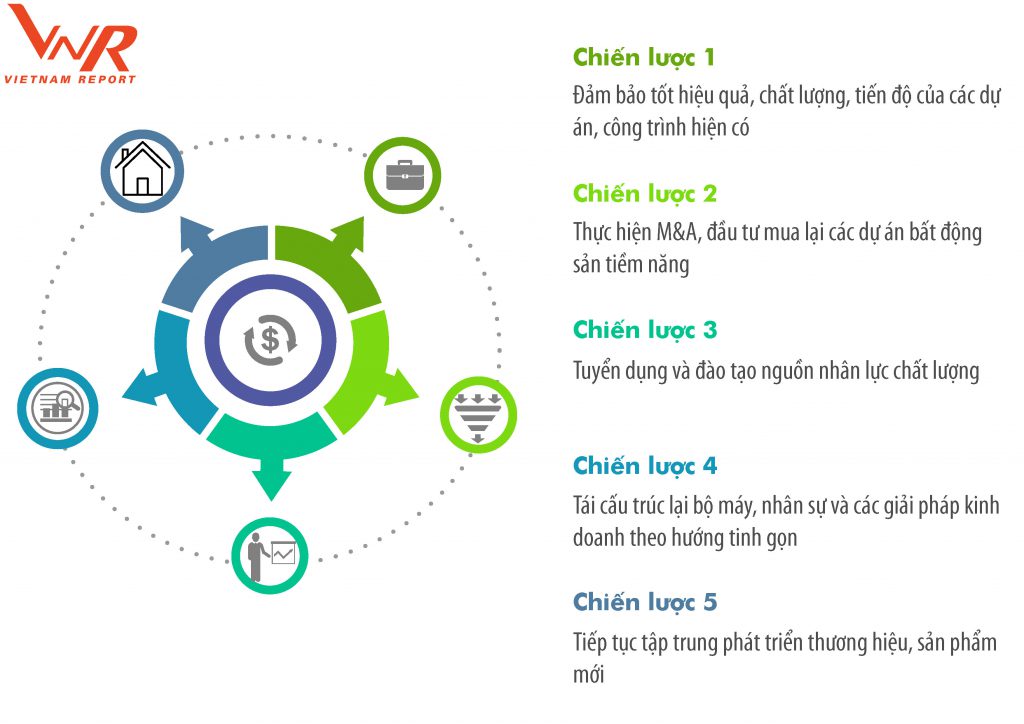

Top 5 priority business strategies in the post-Covid-19 period

The survey of property developers by Vietnam Report have revealed their top 5 priority strategies in the post-Covid-19 period. In addition to efficient and quality delivery of existing projects and development of new brands and products as in previous years, they have devised additional strategic options, including: M&A, acquisition of potential property development projects; talent recruitment and development to respond to the new requirements, and organizational structuring and adoption of lean business solutions.

Figure 9: Top 5 priority strategies of property developers in the post-Covid-19 period

Source: Vietnam Report, Survey of real estate experts and companies, February and March 2021